How Solar Affects Your Homeowners Insurance Roof

How Solar Affects Your Homeowners Insurance Roof

Installing solar panels changes how your homeowners insurance covers your roof. Roof-mounted solar panels fall under Dwelling Coverage, which means they are treated as part of your home’s structure. Understanding how solar affects homeowners insurance for your roof protects you from two real risks: filing a claim that gets denied and carrying too little coverage after installation. The key facts every homeowner needs are here before you sign anything.

How does homeowners insurance cover roof-mounted solar panels?

Roof-mounted solar panels permanently attached to your home are covered under Dwelling Coverage, also called Coverage A. GEICO confirms that insurers treat roof solar panels as part of the home itself, not as separate personal property. That distinction matters because Coverage A carries your highest protection limit and applies to the widest range of perils.

Standard homeowners policies cover solar panels against these sudden and accidental events:

- Fire and lightning strikes

- Hail and windstorm damage

- Theft of panels or components

- Vandalism

- Weight of ice, snow, or sleet

Gradual deterioration and maintenance issues are not covered. If a panel degrades over time, cracks from thermal cycling, or fails because of a poor installation, your homeowners policy will not pay. Openly notes that standard policies cover sudden and accidental damage only. That line between “sudden event” and “gradual problem” is exactly where most solar claims get disputed.

Ground-mounted panels follow a different rule entirely. They fall under Other Structures coverage, also called Coverage B, which carries a 10% cap on your dwelling limit by default. A home insured for $400,000 gets only $40,000 in Coverage B protection. For a large ground-mounted array, that limit runs out fast.

Pro Tip: Tell your insurer whether your panels are roof-mounted or ground-mounted before your policy renews. The coverage category changes, and so does the limit that applies.

Does adding solar panels raise your homeowners insurance premium?

Adding solar panels increases your home’s replacement cost, and that increase requires you to raise your Coverage A limit. Solar systems typically cost $15,000 to $30,000 or more to replace. Carrying the same coverage limit you had before installation leaves you underinsured by exactly that amount.

The premium impact is real but usually manageable. Here is what the process looks like for most homeowners:

- Get a written cost estimate from your installer. Document the system cost, installation date, and mounting method before the crew arrives.

- Call your insurance agent before installation is complete. Do not wait for your annual renewal.

- Request a revised replacement cost estimate. Your insurer needs to recalculate Coverage A to include the solar system’s full value.

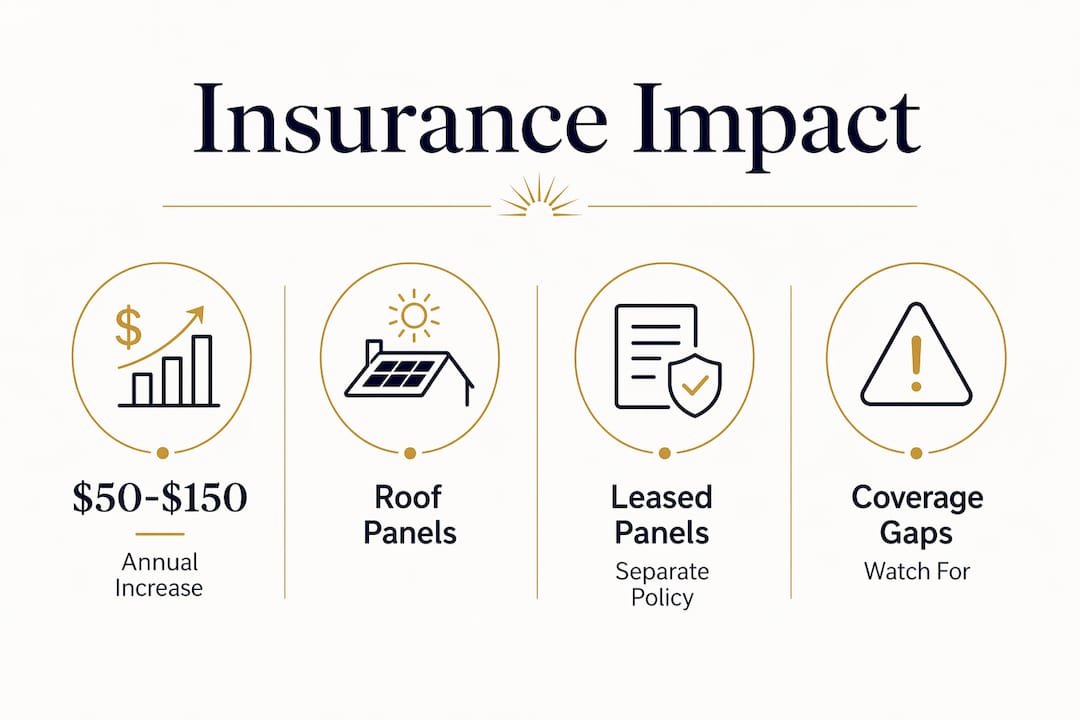

- Review your updated premium. Premium increases typically range from $50 to $150 per year for systems valued between $20,000 and $30,000, though the exact amount varies by insurer and location.

That $50–$150 annual increase is a small number relative to the protection it buys. A $25,000 solar system left off your policy is a $25,000 out-of-pocket loss if a wildfire or hailstorm hits. The biggest insurance risk after going solar is not the premium increase. It is failing to update your dwelling replacement cost at all.

Homeowners commonly assume their policy limits update automatically after a home improvement. They do not. Page Insurance confirms that policy limits do not self-adjust after installation. You must contact your insurer directly.

Owned vs. leased solar panels: who covers what?

Ownership status changes your insurance responsibilities significantly. The rules are straightforward once you know them.

If you own your panels outright:

- You are responsible for updating your Coverage A limit to include the system’s replacement cost.

- Damage from covered perils is paid under your dwelling coverage.

- You file the claim, and your deductible applies.

If you lease your panels:

- The leasing company typically insures the panels themselves under their own commercial policy.

- Your homeowners policy still covers your roof structure.

- You must confirm in writing whose policy covers roof damage caused by or related to the panels.

Leased panel coverage creates a gap that catches homeowners off guard. The leasing company’s policy covers the equipment. Your policy covers the roof deck, rafters, and structure beneath it. If a storm tears panels off and damages the roof, two separate claims may need to be filed with two separate insurers. Knowing this before a storm hits saves weeks of confusion afterward.

Pro Tip: Ask your leasing company for a copy of their insurance certificate. Confirm the coverage dates, the covered perils, and whether roof damage caused by panel removal is included.

Reviewing your solar roofing installation details before signing a lease agreement gives you the documentation you need to have that conversation with both insurers.

What coverage gaps should you watch for with rooftop solar?

Coverage gaps in solar-related roof claims follow predictable patterns. Knowing them in advance lets you close them before they cost you money.

The table below shows the most common scenarios and how standard policies respond:

| Scenario | Covered? | Notes |

|---|---|---|

| Hail cracks panels and damages roof deck | Yes | Covered peril under Dwelling Coverage A |

| Panel degrades over 10 years and fails | No | Gradual deterioration is excluded |

| Installer error causes roof leak | No | Installation defects are not covered perils |

| Wildfire destroys panels and roof | Yes | Fire is a covered peril under Coverage A |

| Flood damages ground-mounted array | No | Flood requires a separate NFIP or private policy |

| Earthquake shifts roof-mounted panels | No | Earthquake requires a separate endorsement |

| Theft of panels from roof | Yes | Theft is a covered peril under Coverage A |

Cause-of-loss coding drives every claim outcome. An adjuster assigns a cause-of-loss code to your claim, and that code determines whether coverage applies. Damage from a covered peril triggers payment. Damage from maintenance failure or installation error does not. When you file a claim involving solar panels, document the cause carefully with photos, weather records, and installer reports.

Equipment breakdown endorsements are worth asking about. Some insurers offer riders that cover mechanical or electrical failure of solar equipment beyond what standard Coverage A provides. This fills the gap between “sudden storm damage” and “panel stopped working.” Not every insurer offers this endorsement, and pricing varies, but it is worth a direct conversation with your agent.

Ground-mounted systems face the steepest coverage gap. The default 10% Coverage B limit rarely matches the replacement cost of a large array. If your ground-mounted system cost $40,000 and your home is insured for $350,000, Coverage B pays only $35,000. You would owe $5,000 out of pocket. Requesting a Coverage B limit increase or a scheduled property endorsement closes that gap entirely.

Understanding solar panel roof clearance requirements also affects how claims are assessed, since improper mounting can shift damage from a covered peril to an installation defect in the adjuster’s report.

Key Takeaways

Installing solar panels requires you to update your homeowners insurance coverage limits immediately, or you risk carrying less protection than your home’s actual replacement cost.

| Point | Details |

|---|---|

| Roof panels fall under Coverage A | Permanently attached roof solar panels are covered as part of your dwelling structure. |

| Update your coverage limit after installation | Solar systems add $15,000–$30,000 or more to replacement cost; your policy limit must reflect that. |

| Premium increases are modest | Most homeowners pay $50–$150 more per year after updating coverage for a $20,000–$30,000 system. |

| Leased panels create a coverage split | The leasing company covers the equipment; you cover the roof structure beneath it. |

| Cause-of-loss determines every claim | Covered perils trigger payment; gradual wear, installation faults, and floods do not. |

What 30 years of solar installations taught me about insurance

Most homeowners treat the insurance conversation as an afterthought. They finish the installation, get excited about their first low electric bill, and never call their insurance agent. I have seen that mistake cost people tens of thousands of dollars.

The part that surprises homeowners most is how simple the fix is. One phone call to your agent before installation, a written cost estimate from your installer, and a coverage limit update takes about 20 minutes. That 20 minutes protects a $25,000 asset for the life of the system.

The leased panel situation is where I see the most confusion. Homeowners assume the leasing company handles everything. They do not. The leasing company covers their equipment. Your roof is still your responsibility. I always tell homeowners to get the leasing company’s insurance certificate and read it before signing the lease, not after.

The other thing worth knowing: a licensed solar contractor who uses in-house crews and pulls proper permits gives your insurer clean documentation. That documentation matters when a claim is filed. An adjuster reviewing a permitted installation with a clear paper trail is far more likely to approve a claim than one reviewing a job with no permit and no records. Installation quality and insurance outcomes are directly connected.

— Curtis Williamson

San Diego Solar and your installation documentation

San Diego Solar has completed thousands of residential installations across San Diego County since 1996, using 100% in-house crews with zero subcontractors. Every installation includes proper permitting, SDG&E interconnection paperwork, and a documented system cost that gives your insurance agent exactly what they need to update your coverage limits.

When you work with San Diego Solar, you get a written project timeline, a clear system cost record, and a crew that has handled every type of roof in San Diego. That paper trail protects your insurance claim before one ever needs to be filed. San Diego homeowners can request a free consultation to get a custom system design and the documentation your insurer will ask for. For homeowners in coastal areas, San Diego Solar’s Del Mar installation team brings the same in-house expertise to every roof.

FAQ

Does homeowners insurance automatically cover solar panels?

Roof-mounted solar panels are typically covered under Dwelling Coverage without a separate policy, but you must notify your insurer and update your coverage limit to reflect the added replacement cost.

Will solar panels raise my homeowners insurance premium?

Yes, premiums usually increase modestly. For systems valued between $20,000 and $30,000, most homeowners see an increase of $50–$150 per year after updating their dwelling coverage limit.

Are leased solar panels covered by my homeowners insurance?

Leased panels are typically insured by the leasing company, not your homeowners policy. Your policy still covers your roof structure, so you need to confirm with both parties whose coverage applies to roof damage related to the panels.

What solar damage does homeowners insurance not cover?

Standard policies exclude gradual deterioration, normal wear and tear, installation defects, flood damage, and earthquake damage. Only sudden and accidental damage from covered perils like fire, hail, or theft triggers a payout.

Do ground-mounted solar panels have different coverage than roof panels?

Ground-mounted panels fall under Other Structures coverage, which defaults to 10% of your dwelling limit. That cap is often too low for large systems, so homeowners with ground-mounted arrays should request a higher Coverage B limit or a scheduled property endorsement.